Hyperin-what?

This piece, written in September 2021, is unfortunately one that I believe might prove to be prescient at some point over the next five years. I say unfortunately because the topic at hand, hyperinflation, is a devastating outcome for almost all of society.

I intend to show what hyperinflation is, how we could get there, what it would look like and then what the fall out could be if it were to happen in todays society. I will focus on the scenario for hyperinflation of the US Dollar, because it’s really the only currency that matters as all others are linked to it. If the USD hyperinflates, then everything else will go with it.

Anyone who follows economics and financial markets is well aware of the heated debate between inflation and deflation. There’s three distinctly different prevailing narratives:-

The deflationists who point to the one thing that supposedly always tells the truth, the bond market, to show that the US Government can continue to borrow money for 30 years at less than 200 basis points. Or even more startling is that the Greek Government can borrow for 20 years at less than 100 basis points.

The Global Central Bank Cabal, who admit that there is some minor inflation in some goods and services, but that the inflation is transitory in nature and they have the tools to combat it should it ever extend beyond their upper band for a period of time that’s outside their comfort zone.

The inflationists who don't buy the deflationist or Central Bank narratives and believe that we have a period of high inflation which is going to be persistent and move the world into a new inflationary regime for the first time in 40 years.

Using the fiercely debated CPI metric as a measure, I would suggest that the three groups predictions on the CPI over the next decade are broadly within the following bands:

Deflationists: CPI at between minus 2% (which is actually deflation, not disinflation) and plus 1%.

Central Bank Cabal: An average CPI of 2% over the long-run, meaning that they will tolerate inflation running above (below) 2% for a period if it in periods years has undershot (overshot) it’s target.

Inflationists: A sustained period of high inflation, beyond 4% and perhaps as high as 10% annually.

Even the most staunch inflationists don’t see a scenario where inflation gets to what Phillip Cagan described as hyperinflation, where prices rise at more than 50% per month. Once currency devaluation gets anywhere near the hyperinflation definition, it makes little difference whether it’s 20% or 1,000% because the notes are worth little more than the paper they’re printed on and it becomes impossible to rectify the situation with anything other than a great reset.

Hyperinflation occurs when there is a complete loss of faith in a currency. Since 1971 when President Nixon took the USD off the gold standard, we have been in an era of pure fiat currency. Fiat currency means “currency issued by the relevant body in a country or by a government that is designated as legal tender in its country of issuance through amongst other things, government decree, regulation, or law.”

The word fiat is a Latin word that translates broadly to ‘let it be’. Essentially, it means that one USD is worth one USD because the government says that is so. More important than the government saying it is so is the market believing them – which is why we have seen many instances of hyperinflation in jurisdictions where the public loses faith in their authorities and no longer believes their word that the unit of issued currency is worth what they say.

Perhaps the most famous example of hyperinflation was that which occurred in Weimar Germany in the early 1920’s. Money became worthless, which meant so were the savings denominated in marks that so many middle class people had relied upon. A wealthy class who had close ties with the Central Bank could borrow soon to be worthless money to buy hard assets (everything from houses, factories or grand pianos) from a starving working class who would sell whatever they could to buy their family their next meal.

Hugo Stinnes, a German industrialist did so well for himself during these times that he earned the nickname Inflationskonig - the Inflation King. It is no coincidence that this website shares the same name – a constant reminder of what can happen when a nations currency is debauched.

Adam Fergusson explained that “in hyperinflation, a kilo of potatoes was worth, to some, more than the family silver; a side of pork more than the grand piano” in his excellent book on the topic, When Money Dies. The book includes many quotes from people who lived through these times and explain what it was like. This following recollection shows exactly why the National Socialist Party was democratically elected a decade after the nightmare.

“My allowance and all the money I earned were not worth one cup of coffee. You could go to the baker in the morning and buy two rolls for 20 marks; but go there in the afternoon and the same two rolls were 25 marks. The baker didn’t know how it happened… His customers didn’t know… It had somehow to do with the dollar, somehow to do with the stock exchange – and somehow, maybe, to do with the Jews.”

Right now that is the case in places like Venezuela, Zimbabwe, South Sudan, Argentina and Iran. When the people stop believing that a Venezuelan Bolivar is worth what they’re told it is, it becomes one big game of hot potato where the population will exchange that soon to be worthless paper for whatever hard goods or currency they can get their hands on. No one wants to get caught holding a bag of completely worthless paper.

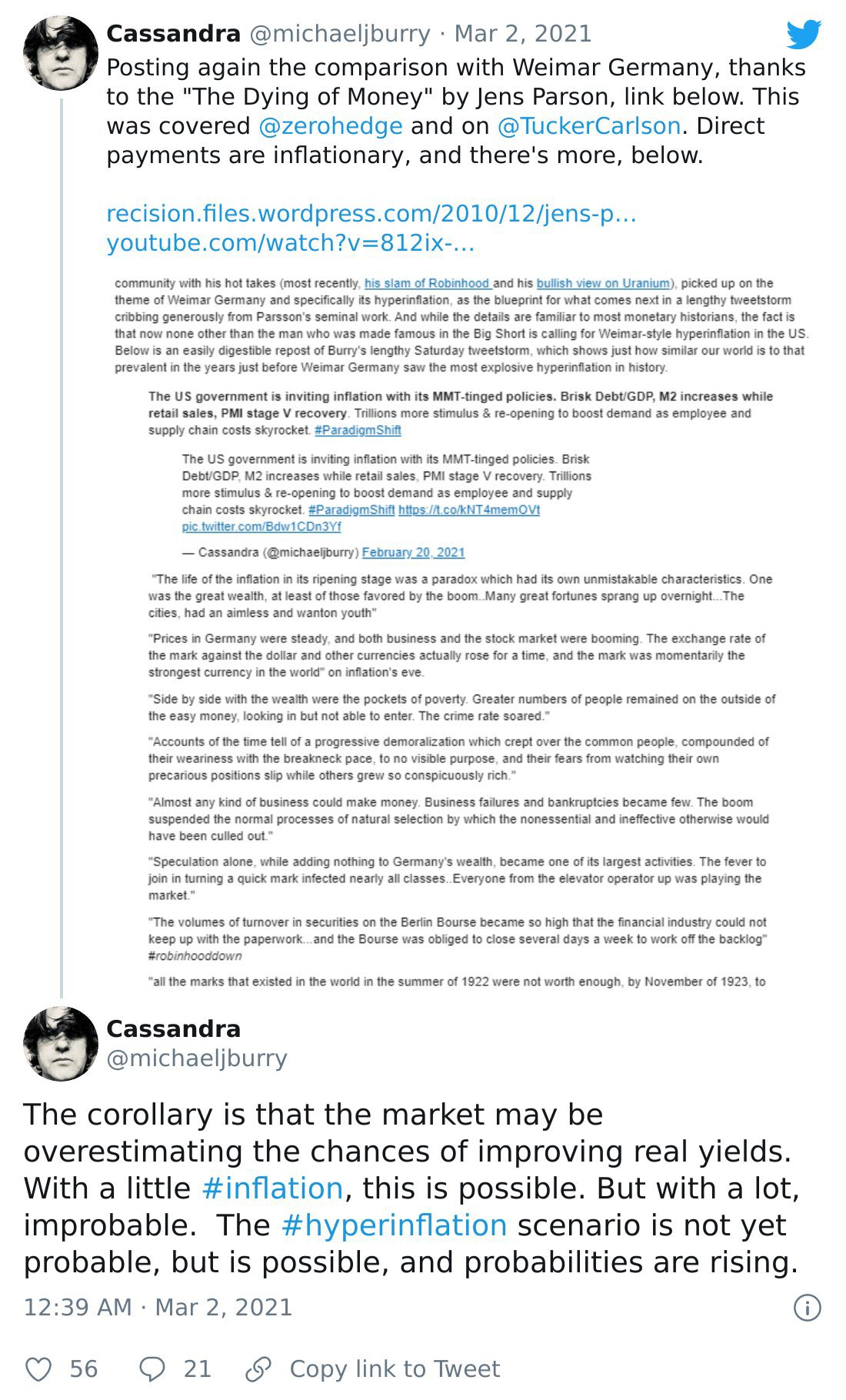

Hyperinflation in the developed world is a scenario that most pundits believe could never happen. But there’s at least three people who have mentioned it as being a possible outcome and all three of those are people with a fine track record of predicting the future.

Michael Burry, the man made famous by Christian Bale in The Big Short for predicting the GFC, started ringing the alarm bells on hyperinflation in March this year. Two weeks later, Burry took a break from Twitter.

Professor Richard Werner, one of the worlds leading experts on global banking and the inventor of the now misused quantitative easing has issued similar warnings to Burry over the past 12 months with a prediction that Weimar Germany 1923 = America 2023.

The third person who has issued the hyperinflation warning is a man who remains one of the leading figures in the Deflationist camp, Dr Lacy Hunt. Hunt, whose Hoisington Investment Management has been one of the best performing bond funds over 4 decades, continues to see deflation on the horizon with one proviso: If the Federal Reserve Act is changed to give the Fed the power to spend, Gresham’s Law would prevail and it would result in hyperinflation.

An entire thesis could be written on the Central Bank policy of quantitative easing and whether it does or does not lead to inflation. In the spirit of brevity, I am going to attempt to distill the implications of what Central Bankers have been doing over the past two decades in just a few simple paragraphs.

Now we should note that the Central Bankers and Private Bankers are more or less the same people. Former Fed Chair, Janet Yellen, earned $7M in speaking fees from the same private banks she supposedly regulated during her two year hiatus before she took up her current gig as Treasury Secretary, replacing the former Goldman Sachs executive Steven Mnuchin. It’s much the same story for Ben Bernanke, Alan Greenspan et al.

Since the GFC, they’ve all engaged in one round after another of quantitative easing. We’re told its money printing, most of the market and media believes it is money printing and we all go along with the narrative. The mechanism, as we’re told, is that the Central Banks print money to buy financial assets (primarily government bonds) from the private sector. This essentially moves this newly created money into the real economy via primary dealers (special banks with privileges to deal with the central bank directly, who also pay former central bankers healthy speaking fees) who sell their financial assets to the Central Bank. In times of crisis (eg the GFC or March 2020), they will buy distressed financial assets (like mortgage backed securities or junk bonds) at face value in order to keep the banks from going under and therefore maintaining market stability.

For example, the US Government wants to raise money to fund a deficit spending program and auctions newly issued 10 year government bonds to their network of primary dealers (Goldman Sachs, JP Morgan, Citigroup etc). In a collateral based financial system, primary dealers love off-the-run treasury securities given the value they can extract from them as a balance sheet tool. They become even more valuable in a quantitative easing regime given that they can on-sell these treasuries to the Central Bank, which is a guaranteed buyer of these securities at a higher price than that which they paid for them at auction.

We can see that QE has led to $20+ trillion in central bank balance sheet expansion in just over a decade. The noble lie that we’re told is that the Central Bank prints new money to buy these securities, but this is not true. What they are printing is new bank reserves, which are securities held by private member banks at the Central Bank. They’re a balance sheet asset, just like a treasury security. A bank reserve is not cash, it cannot be used as legal tender. All thats really happened during this QE process is a series of complicated asset swaps or accounting processes – no money printing.

This is a point that deflationists bang on about – that the whole QE process is one big illusion that is designed to jawbone financial markets into thinking that the otherwise impotent Central Bank has their backs. I don’t fully agree with this sentiment and I think that QE has had some serious implications for financial markets.

I think it’s done two key things. Each is an essay in its own right, but I’ll oversimplify it here so as to not get bogged down.

It’s driven up the value of collateral in the financial system, which has increased the wealth of anyone owning collateral (primarily private banks) and by extension increased the purchasing (and therefore price) of other assets (like equities) due to the rebalancing effect within passive portfolios. Explained best by Mike Green in this interview.

It suppresses the most important figure in global finance, the risk free rate. The price of capital in the entire credit market is derived from the risk free rate. Whether thats the US Government, the Greek Government, the mortgage market or Hertz issuing junk bonds – every single figure is influenced by a rate that is being artificially suppressed. More on this topic from Doomberg here.

The end result of 15 years of QE and $20+ trillion in new bank reserves?

An asset bubble in every, single market.

A complete failure to create new credit for productive investments (eg real economic growth).

Liquidity being trapped in the financial system and never reaching the real economy.

A global economy completely broken and totally controlled by private bankers.

And yet still, anemic inflation.

The banking cabal are not silly. They are well aware that the general public is growing tired of all this money printing that never seems to reach their own hip pocket. And whilst they’ll never admit that their strategies were never going to help the common person in the first place, they are shifting their current narratives to suggest that we might’ve reached the limits of monetary policy’s ability to impact the real economy.

For at least the last 12 months, we’ve heard both the Fed and ECB talk about the importance of fiscal stimulus in supporting an economic recovery. Of course, the role of the Central Banks is simply to keep financing conditions favourable and they are limited in their power to get money into the hands of those who need it.

There’s a problem with the structure of our global banking system when it comes to getting new money from credit creation into the hands of those who need it. Those who benefit most from new credit creation are SME’s. As this paper shows, “small and medium-sized enterprises, in aggregate, are the biggest employer in most countries, accounting for about two thirds of all employment in the UK, more than 70% in Germany and about 80% in Japan.”

The same paper also shows empirically a point that makes complete sense both logically and anecdotally – SME’s do not get loans from the Primary Dealer type banks who feed off QE like Goldman Sachs. But rather, there is “an inverse relationship between bank size and the propensity of banks to lend to small businesses”. With the Central Banks at the end of the road in terms of their ability to generate productive credit creation for SMEs – maybe we will see a set of policies that bypass the banking monopolies and promote the establishment of smaller not for profit community banks?

I doubt it, but I’m also a cynic. Maybe I’m wrong and this is exactly what happens – bubbles in financial markets start to deflate, global banking cartels reduce their power, small businesses flourish, the working class people get full time jobs with local firms.

If you believe this is what will happen, you can stop reading now. But read on for my views on what will actually happen.

I believe we see (or continue to see) the following trends:

The continuance of QE and other policies to create favourable financing conditions fails to impact the real economy.

Despite warning that they will do so, the Central Banks fail to implement any form of tapering because we all know that asset markets cannot stand on their own two feet.

Distortions in the price of everything continues to present issues for policy makers. House prices rising 37% annually in states like Idaho or shipping rates multiplying by a factor of six creates all sorts of societal issues.

These issues dial up the already tense pressure valve on the idea of QE for the people from ‘progressives’ and the Central Bank controlled media.

With these factors building up, we’re infinitely close to the point Lacy Hunt warns about where it becomes apparent (and beyond argument or jawboning) that even an astronomical increase in debt (eg more QE) does not produce a sanguine result.

The Central Banks will correctly say that they are hamstrung by legislation like the Federal Reserve Act, just like Jay Powell stressed last year.

“I would stress that these are lending powers, not spending powers. The Fed is not authorized to grant money to particular beneficiaries. The Fed can only make secured loans to solvent entities with the expectation that the loans will be fully repaid.”

With these restrictions in place, the attempt to generate productive credit creation and therefore economic growth is like pushing on a string. Danielle DiMartino Booth used this analogy in an interview with Lacy Hunt where she asked him if this ‘frustration’ causes the Central Banks to ‘cross a line’ and change the Federal Reserve Act, enabling them to spend.

Lacy’s response was that in that case, you would have a regime change where you are indeed printing money and in very short order you will get hyperinflation. In my view, this is the crux of the issue – we’re on a road that’s leading to an almost inevitable end game where the central banks actually print money and it truly blows up the currency.

So what would it all look like?

The good thing about analysing a hyperinflation event is that unlike high inflation, low inflation or disinflation – there’s far less ambiguity. It’s devastating in its effects, but it also creates clear outcomes.

In hyperinflation, something that costs you $100 today (say a full tank of fuel) might cost you $200 tomorrow and $400 the day after. The currency hasn’t gone up, the prices have gone up and therefore the value of each currency unit has gone down. In inflationary environments it’s often said that the cure for higher prices is higher prices. Hyperinflation is different, because the psychological effects of believing that your currency is worth less tomorrow causes you to get it out of your hands today, therefore creating a reflexive feedback loop that sends prices infinitely higher.

This has profound impacts for the currency in circulation. Savings (bank deposits, physical cash, or fixed income/bonds) become worthless. Fixed rate debt obligations (private debt like mortgages or public debt) are cleared.

The price of real assets appreciate exponentially in nominal terms. That includes equities, real estate, precious metals, commodities, collectibles or anything else that the market deems to have more real value than their worthless paper.

Although we look back retrospectively on daily or weekly hyperinflation rates, the reality is that society ceases to function. When one loses complete faith in the value of their currency, their focus shifts to the necessities like how they’re going to pay for food, energy and water. We got a glimpse of how society looks with the toilet paper shortages throughout 2020 – now imagine if people were forced to fight over the last can of beans that are selling for the same price as their last years salary?

It’s easy to think that hyperinflation could have its benefits – like for the real estate owner who has cleared their now worthless debt and has unencumbered possession of their property. The challenge is that the same person is in desperate need of other vital supplies and might need to dispose of their home in order to pay for those goods. Anyone who has studied negotiation knows who holds the power in that transaction.

Maynard Keynes knew that the process of creating a hyperinflationary event was a tactic that the Bolshevik’s might use to destroy a society and usher in their preferred communistic regime when he reflected on his learnings from Vladimir Lenin in the mid 1910’s.

“Lenin is said to have declared that the best way to destroy the Capitalist System was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some.”

Hyperinflation would benefit the talented bankers and speculators who understand what is happening, have the resources and know how to exploit it. Do we think that the Primary Dealers will get stuck holding the worthless government bonds, or will they be able to wait until exactly one minute to midnight before shifting them to the Central Banks balance sheet on whatever terms they deem suitable?

It would destroy everyone else. We can consider the question posed by Adam Fergusson to think about how simultaneous hyperinflation globally might impact the world today.

“The question to be asked – the danger to be recognised – is how inflation, however caused, affects a nation: its government, its people, its officials, and its society. The more materialist that society, possibly, the more cruelly it hurts.”

Some people believe that the regime change that triggers it will be the introduction of Central Bank Digital Currencies (CBDCs), which effectively gives citizens their own bank account at the Central Bank and allows a transmission of money that bypasses the banking system and therefore equates to direct money printing or monetisation. I don’t hold that view – I believe that CBDCs will be ushered in as the solution to the chaos and instability caused by hyperinflation.

There would be little opposition to the implementation of CBDCs and whether we want to create a new currency that is totally controlled and surveilled by the same cabal that got us into the mess in the first place.

Every global citizen can go online and register their CBDC account, which would be preloaded with a nominal balance for every person. ECB President Lagarde has been priming us for years, explaining that “The advantage is clear. Your payment would be immediate, safe, cheap and potentially semi-anonymous... And central banks would retain a sure footing in payments.”

Trade resumes. Society is restored. The bankers organise a big conference and “seize this new Bretton Woods moment” to reorganise the ownership of global resources and assets. You and I won’t be included in that ownership though, my friend.

Never let a good crisis go to waste.

The Federal Reserve funded financial institutions like Blackstone will own the real estate market.

“Blackstone built its rental-home business with an advantage few if any other buyers could match: billions of dollars in credit from large banks. Its Invitation Homes subsidiary quickly became the largest single-family home landlord in the U.S., with 50,000 properties. Altogether, hedge funds, private-equity firms and real estate investment trusts have raised about $20 billion to purchase as many as 200,000 homes to rent.”

Larry Fink’s BlackRock won’t miss out on the action either.

Bill Gates will continue his quest to own all of America’s farmland.

But according to these same corporatists who wish to own the worlds assets and dictate top down to us, we shouldn’t worry as we’ll own nothing and we will be happy.

As I write this words, I wish I conclude with my recommendations on what we could do to stop this and reverse the course of history, but unfortunately I think that we’re too far gone. We’ve ceded unassailable control to an elite class of bankers and globalists who I suspect have deliberately got us to this point.

All I hope is that it’s not too long before we the people wake up to what is going on. We realise that the us vs them battles we fight every day on issues like race, sex and creed are being deliberately fuelled by these same corporatists who own the financial system and global media. We realise that the real them is the globalists who see us as little more than expendable sheep as they usher in a new era of Bolshevism.

Wake up people, or it might be too late.